The Enigmatic College Financial Conversation: Navigating the Maze of Timing and Practicality

Parents often find themselves lost in a fog of confusion when it comes to determining the right time to initiate the college financial conversation. Here at college career consulting, we firmly believe that this crucial dialogue should begin early, even as early as freshman year, and be revisited frequently throughout the high school years. We understand the need for practicality and recognize that information is best delivered in small, digestible pieces. In fact, we sometimes yearn for a Monopoly for college game that could simplify this complex process.

Allow us to illustrate the importance of early discussions with a story where parents unknowingly pushed this topic aside, assuming they had ample time to address it. Little did they know that their decision would set off a chain of events leading to an unforeseen twist in their son’s college journey. Brace yourself as we unravel this tale of discovery, challenges, and unexpected turns.

Jimmy’s Story

Their son, Jimmy full of excitement and anticipation, had already accepted an offer to attend a prestigious university. With dreams of campus life and a summer filled with shopping sprees, he was on cloud nine. The countdown to the start of her college adventure had begun.

But just a month before he was set to embark on his university experience, his parents finally decided to have “the talk.” They sat him down to discuss the daunting topic of loans and the hefty price tag attached to his chosen institution. He has just assumed that the parents where going to pay for his education but instead he discovered that they going to help him get a loan. It was a shockwave that rattled his world.

Overwhelmed and uncertain, he sought guidance from us, desperate to understand the implications of each loan and the long-term consequences of his financial decisions. As he unraveled the intricate web of loan jargon, a sinking feeling settled in his gut.

In a moment of clarity and determination, he made a bold request. He asked us to find him a more affordable college option, one that aligned with his preferences and wouldn’t drown him in a sea of debt. Deep down, he worried about disappointing his parents with a change of heart, so he kept his thoughts to himself as he worked tirelessly with us.

With unwavering determination, he refused to carry an overwhelming burden of debt on his shoulders. Together, we scoured the vast landscape of colleges and universities, seeking a hidden gem that could offer him the major he desired at a fraction of the cost. And lo and behold, we discovered a shining star of a college that fit the bill.

This newfound institution promised him the same quality education, catered to his passions, and would cost a staggering 70% less than his previous choice. It was a revelation that filled him with a mix of relief, excitement, and a tinge of trepidation. Yet, he knew deep in his heart that this decision was right for his future.

Gradually, he mustered the courage to share his newfound discovery with his parents, unsure of how they would react. But to his surprise, they embraced his decision with open arms, their love and support shining through. They realized the significance of his desire to avoid drowning in the sea of debt and admired his commitment to financial responsibility.

And so, he embarked on his college journey once again, armed with a newfound sense of empowerment and financial wisdom. The emotional disaster that could have unfolded was averted, thanks to his determination and the discovery of a more affordable college path.

Dear parents, heed this cautionary tale. Don’t underestimate the importance of starting the college financial conversation early on. The consequences can be both emotional and financial. Empower your student to make informed decisions and consider all options, for it is through these conversations that dreams can flourish without the suffocating weight of debt.

Some Key Findings

According to Finmasters:

- Approximately 1 in 7 Americans (13.5%) has student loans.

- The average federal student loan debt per borrower in 2022 is $37,667.

- The highest number of borrowers are aged 25-34.

- 2.5 million Americans in their 60s and older are still paying off student loans.

- Most borrowers need up to 20 years to pay off their student loans.

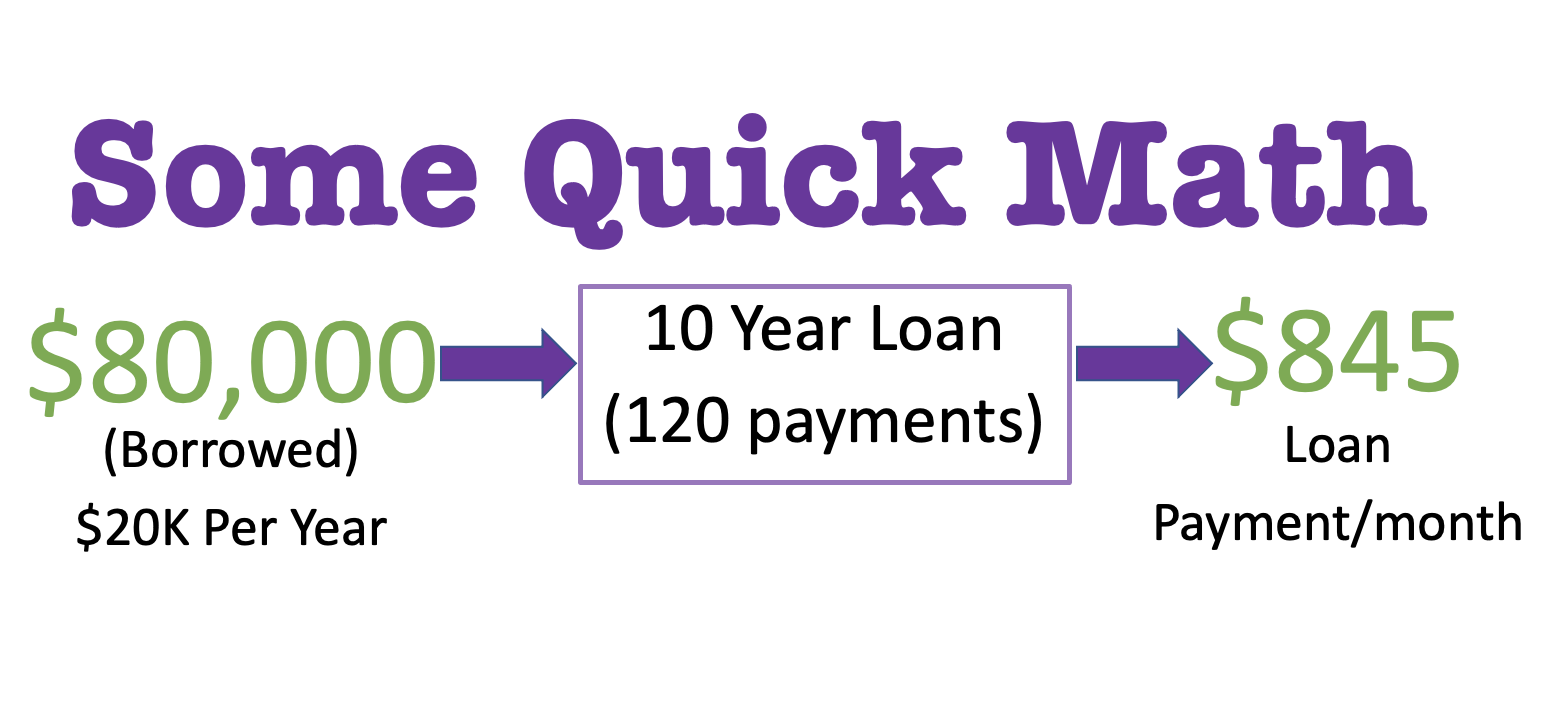

Let’s just say your student conservatively borrowed $20K/year … after he or she graduates they would owe $845/month over 10 years. Wowza! Studies show that students put their ‘dream period’ on hold because of their student debt.

US Student loans taken out for the 2023-2024 school year will have higher interest rates. On the day this blog was posted subsidized and unsubsidized federal loans will carry a 4.99% interest rate for undergraduate borrowers, and 6.548% for graduate borrowers. PLUS loan interest rates are at 7.54% for the upcoming school year for undergraduate and graduate borrowers.

To help you calculate what your student will owe, use the loan repayment calculator.

{kind=link}